Michael Rudolph

Friday, January 12, 2024

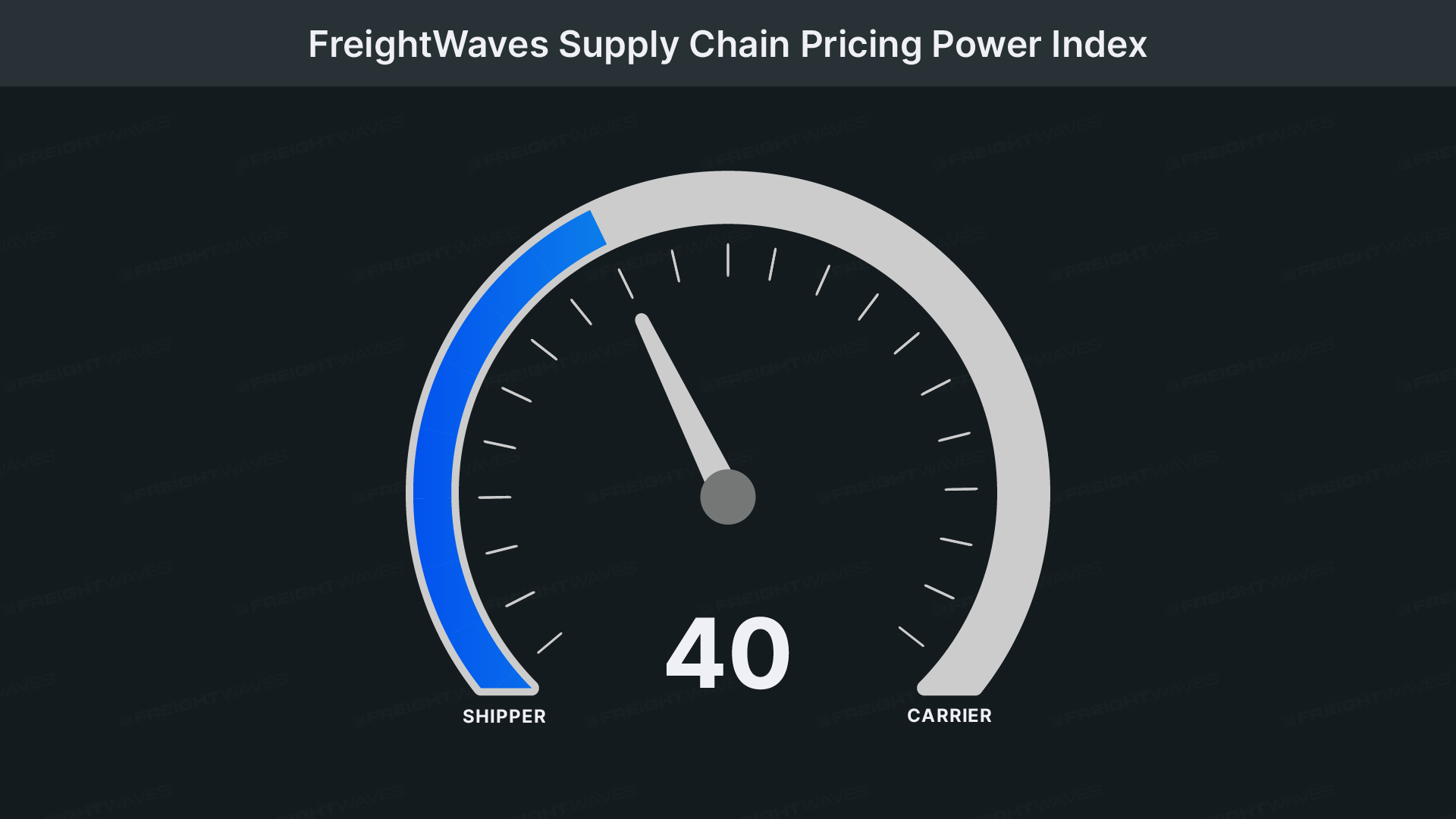

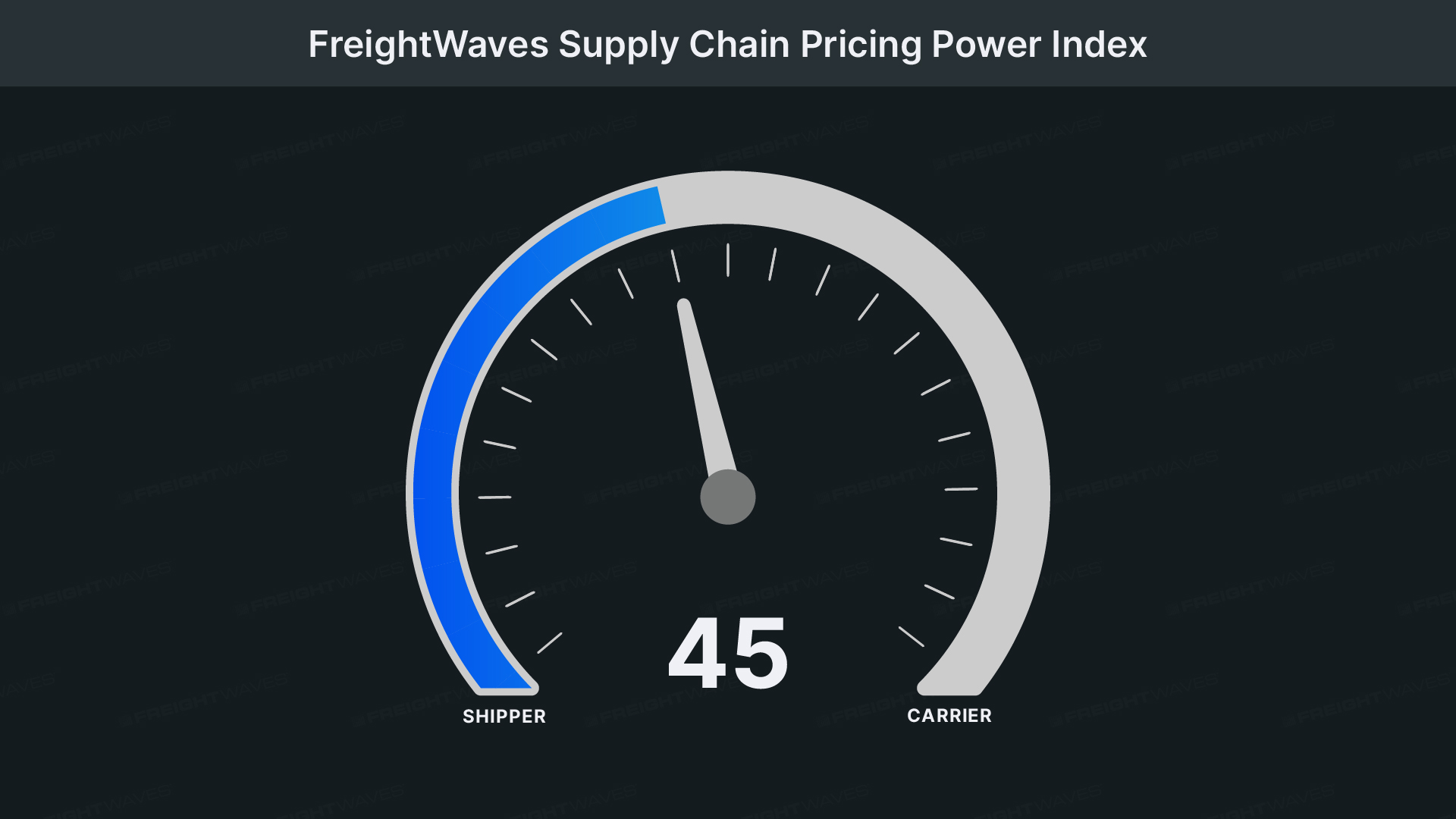

Crosswinds threaten soft landing

The sustained imbalance between supply and demand has yet to be corrected, such that only an unprecedented tidal wave of demand could satisfy the current amount of capacity in the national freight economy.