This week’s FreightWaves Supply Chain Pricing Power Index: 45 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 45 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 40 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

The Pricing Power Index is based on the following indicators:

Freight flow is weakened by sluggish demand from consumers

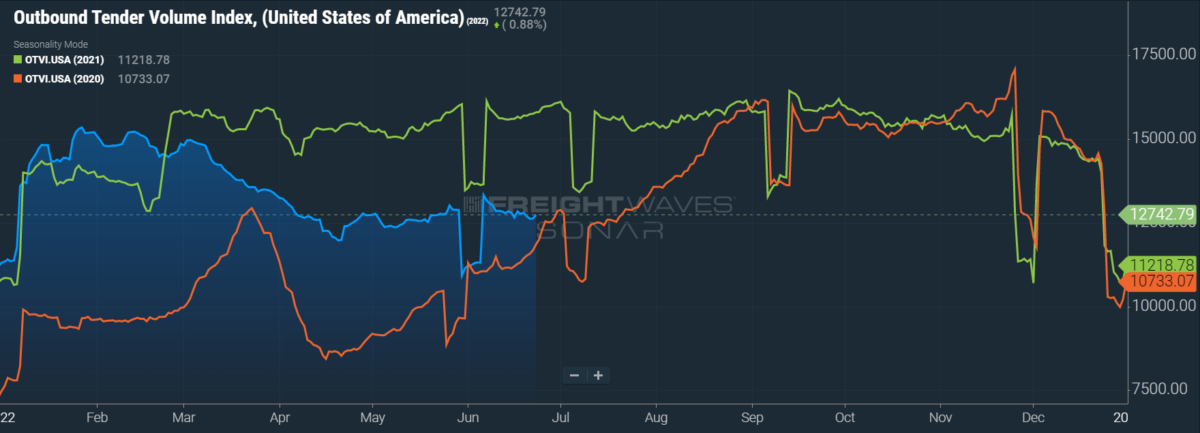

The window between Memorial Day and the Fourth of July is traditionally a strong period for moving freight, in part due to elevated consumer activity in the summer shopping season. This summer, however, has seen freight demand remain static: Both the Outbound Tender Volume Index (OTVI) and true shipment flow are still below year-ago levels.

SONAR: OTVI.USA: 2022 (blue), 2021 (green) and 2020 (orange)

To learn more about FreightWaves SONAR, click here.

OTVI rose a slim 0.67% on a week-over-week (w/w) basis as retailers contend with overstocked shelves and reduced discretionary spending from consumers. On a year-over-year (y/y) basis, OTVI is down 19.41%, although y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

SONAR: CLAV.USA: 2022 (blue), 2021 (green) and 2020 (orange)

To learn more about FreightWaves SONAR, click here.

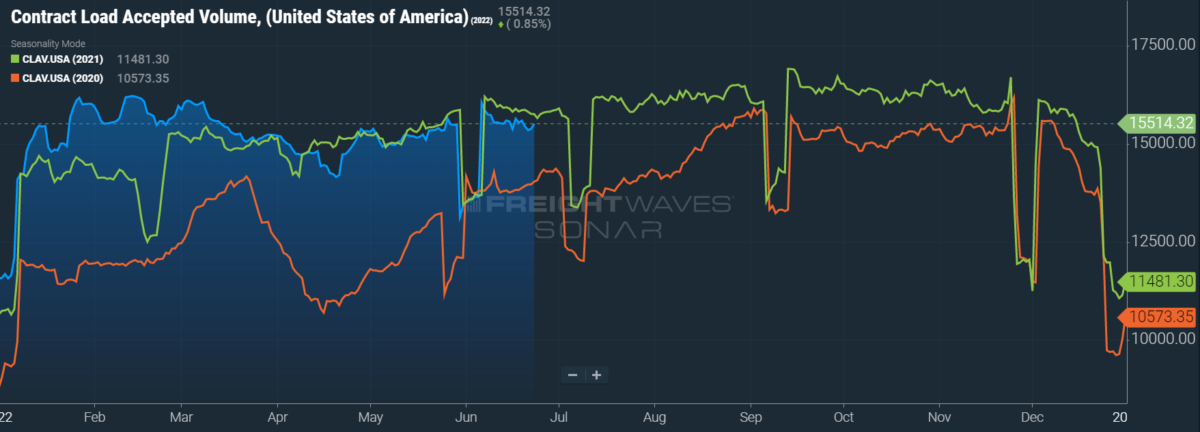

Contract Load Accepted Volumes (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see not only an expected dip of 2.26% w/w but also a further dip of 2.8% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI to lower levels.

The annual State of Logistics Report, released by the Council of Supply Chain Management Professionals, corroborated what many shippers already knew from personal experience: Logistics was expensive last year. According to the report, the total cost of logistics — including transportation, warehousing and other ancillary costs — rose 22.4% y/y in 2021. At a little more than $1.847 trillion, the total amount spent on logistics in 2021 came to represent 8% of the nation’s overall GDP, a level not seen since 2008.

The report also cautioned the logistics sector about the possibility of “a revenue-diminishing and inventory-swelling downturn.” Such a possibility has come into sharper focus as major retailers reported higher-than-expected levels of inventory in their quarterly earnings reports. In addition to inflationary pressures squeezing their consumer base, many retailers are also suffering from shoppers electing to spend more on services than goods.

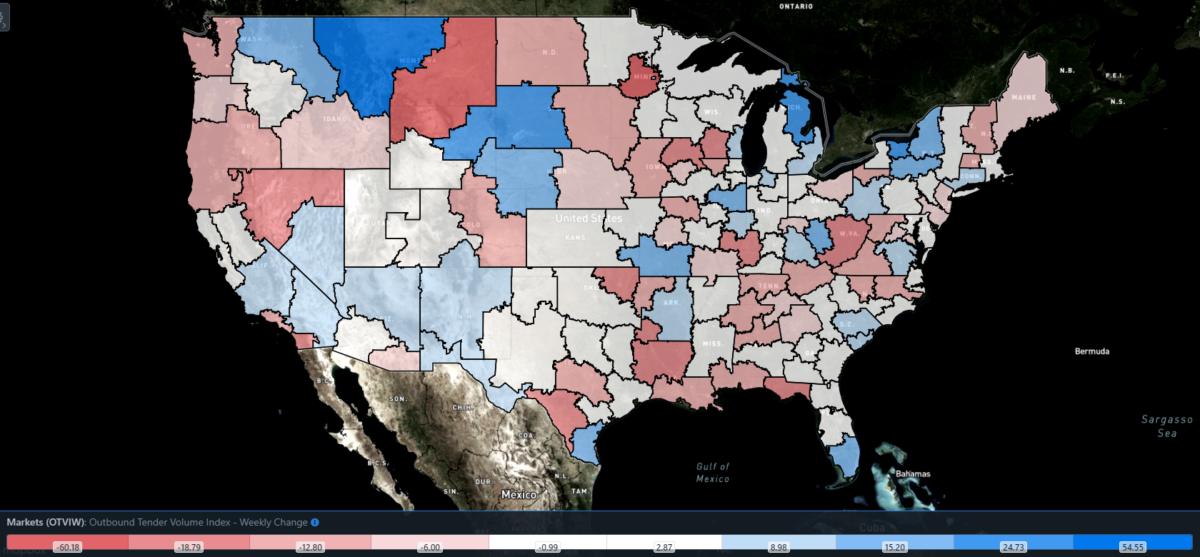

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 73 reported weekly increases. These w/w increases mostly occurred in smaller markets.

One important exception, however, was Ontario, California, which is once again the nation’s largest freight market by outbound volume. Ontario’s freight mostly comprises imports from the nearby Ports of Los Angeles and Long Beach. Most of this week’s over-the-road volume is due to imports that arrived a few weeks prior.

On Thursday, Drewry released its weekly spot rate assessment, which showed rates along the Shanghai-Los Angeles lane are down 7% y/y despite being up 32% y/y last week. These rates have fallen even in the face of a dramatic increase in the cost of marine fuel — as well as all petroleum products — signaling that demand for trans-Pacific shipments is contracting.

By mode: Reefer volumes saw a slight dip this week but nothing too alarming. Strangely enough, it appears that reefers this year were more valued for their temperature-regulating abilities in the winter than their more commonly valued capacity to move fresh produce in the summer. The Reefer Outbound Tender Volume Index (ROTVI) is down a slim 0.63% w/w.

In a reversal of recent trends, van volumes are responsible for much of the downward pressure on the overall OTVI this week. The Van Outbound Tender Volume Index (VOTVI) tumbled 1.57% w/w and is down 21.46% y/y, though much of both ROTVI and VOTVI’s poor y/y performance can be attributed to declining tender rejections.

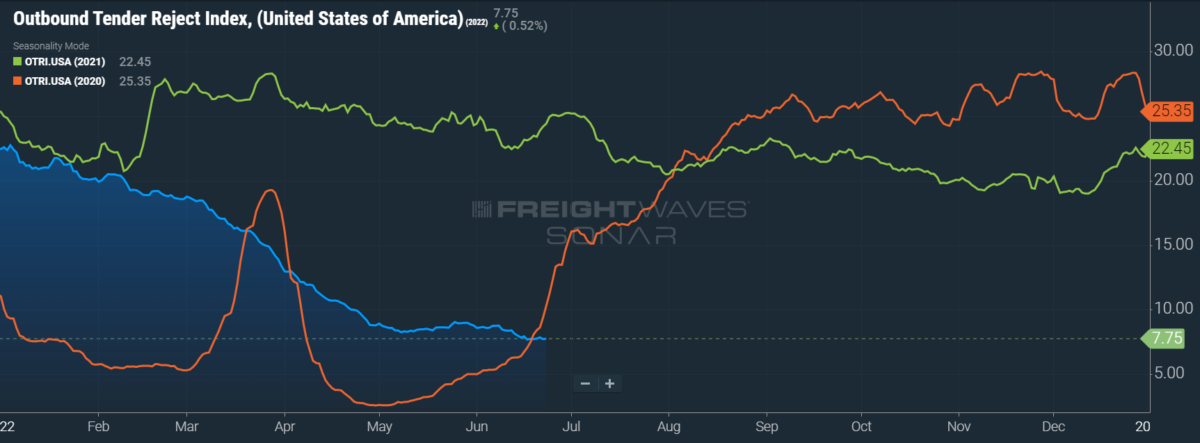

Rejection rates continue to fall after breaking under 8%

Over the past few months, OTRI had been bound between 8% and 9%, leading some observers (including myself) to believe rejection rates had found a new floor for the foreseeable future. Last week, however, OTRI finally dipped below 8%, meaning all bets were off about the degree of future downward movement. This week, OTRI has indeed fallen further, which could signal that breaking the barrier around 7% could be much easier than 8%.

SONAR: OTRI.USA: 2022 (blue), 2021 (green) and 2020 (orange)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 7.75%, a change of 18 basis points (bps) from the week prior. OTRI is now 1,667 bps below year-ago levels.

In 2019, when the industry was undergoing a recession, OTRI at its lowest fell under 4%. Now in 2022, not only the trucking industry but also the broader economy are facing the possibility of a recession. The lowest reading of OTRI, measured on April 30, 2020, was 2.57%. It remains to be seen whether the gathering headwinds will push OTRI below that level.

To make matters worse, 77% of U.S. container imports — as of June 15, 2022, and measured in twenty-foot equivalent units (TEUs) — are coming for industries that already reported massive inventory gluts in their latest quarterly earnings reports: retail, electronics, furniture, clothing and appliances. Many of these products take up a good deal of physical space, which is worsening given the ongoing limitations of current warehousing capacity.

Retailers with overstocked backrooms are left with a bitter choice — either pay the premiums to store their products in warehouses or sell products at a heavily discounted price to entice a consumer base becoming exhausted by inflation. Carriers obviously will hope for the latter scenario so goods continue to move.

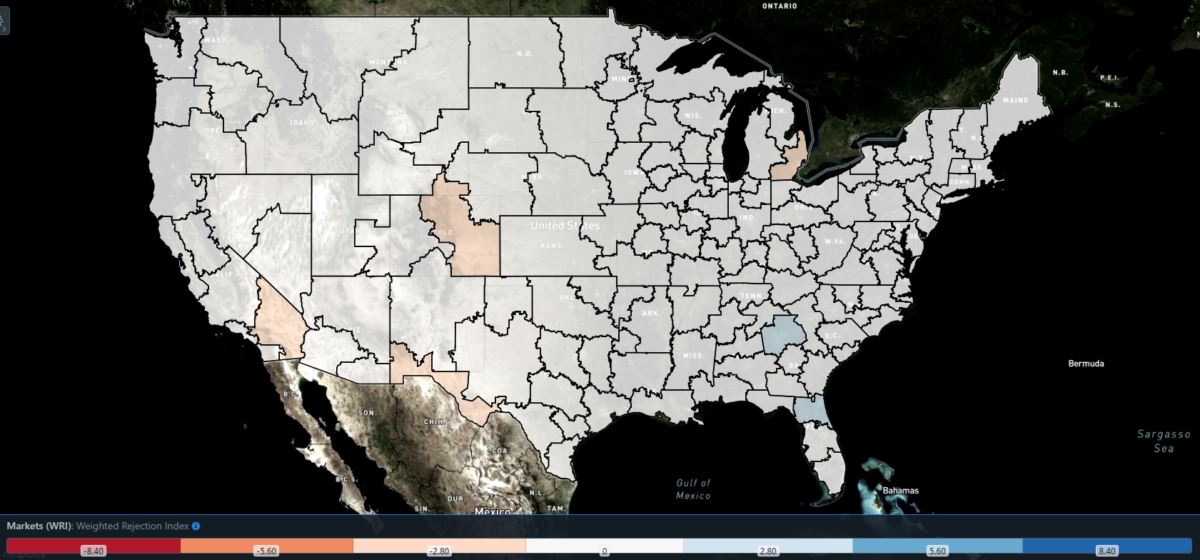

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight, only a few regions this week posted blue markets, which are the ones to focus on.

Of the 135 markets, 64 reported higher rejection rates over the past week, though nearly half only posted increases of 50 or fewer bps.

Atlanta, which saw volumes drop 4.38% w/w, was hit by tender rejections rising 92 bps w/w to 8.75%. On Tuesday, Atlanta’s outbound rejection rate jumped from 7.42% to 8.58%, its largest single-day rise in over a year. In addition to being a large hub for manufacturers and the second-largest market for overall outbound volume, Atlanta holds the distinction of being the fifth-largest outbound market for reefer volume.

To learn more about FreightWaves SONAR, click here.

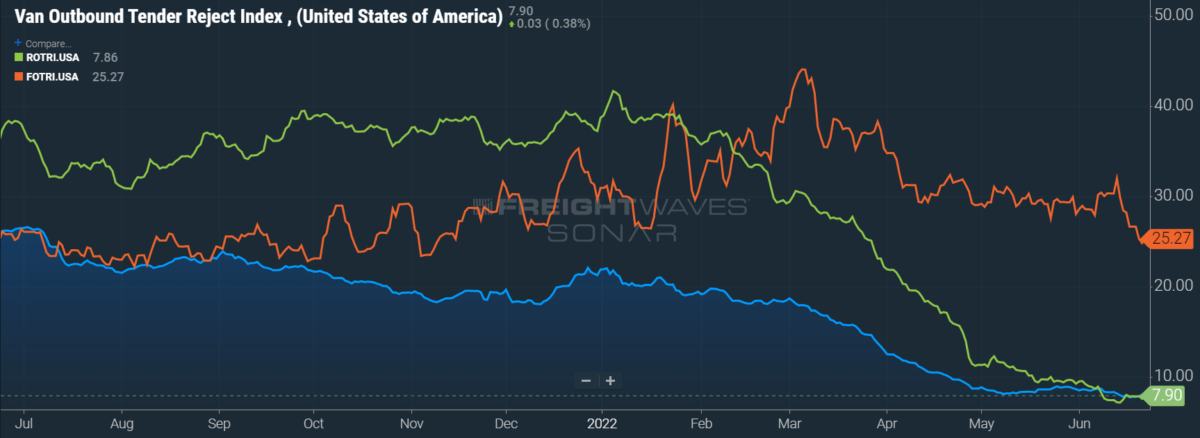

By mode: Flatbed rejection rates, which have been the most robust — if inconsistently so — across all modes, took a steep tumble this week. The Flatbed Outbound Tender Reject Index (FOTRI) fell 293 bps w/w to 25.27%, compounding last week’s decline of 183 bps w/w. Nevertheless, FOTRI alone is still close to year-ago levels, up only 14 bps y/y.

However, flatbeds are not exempt from the gathering economic headwinds. Housing starts fell to their lowest levels in 13 months, suggesting the red-hot housing market is cooling. That should come as little surprise: According to Freddie Mac, the average 30-year fixed rate mortgage has risen 270 bps since the start of the year to 5.81%.

Reefers, meanwhile, are posting the lowest rejection rates across all three modes. The Reefer Outbound Tender Reject Index (ROTRI) fell 13 bps w/w to 7.86%. The Van Outbound Tender Reject Index (VOTRI) is not much better with a drop of 5 bps w/w to 7.90% but still 15 bps above the overall OTRI.

Contract rates finally tumble as spot rates slip ‘n’ slide

Spot rates continued to edge downward Sunday but remained flat for most of the remaining week before dipping again Thursday. Given the National Truckload Index (NTI) is inclusive of fuel, it is an open question whether rising diesel prices will prevent it from falling further or if the slim pickings on the spot market will lead carriers to haul loads at an even lower rate.

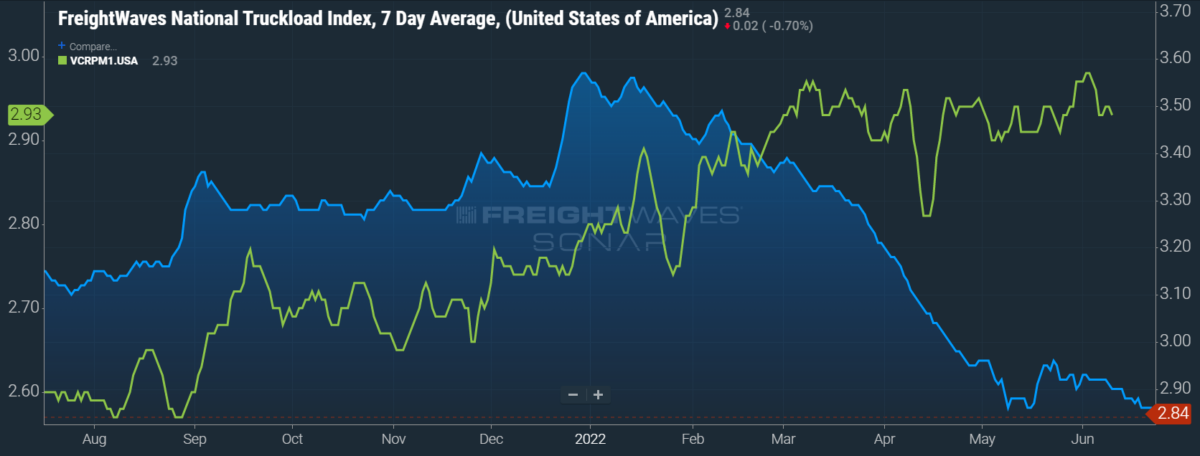

SONAR: National Truckload Index, 7-day average (blue; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

Over the past week, the NTI has fallen 4 cents per mile to $2.84/mi. In the previous year, spot rates climbed steadily over the summer until plateauing in September. Needless to say, the present decline in rates is both unseasonable and foreboding.

The NTIL, which is the linehaul rate that removes fuel from the all-in NTI, also fell 4 cents per mile to $1.95/mi, indicating nearly a third of spot rates are going straight to fuel payments. As expected, any changes in the NTI are due to declining linehaul rates.

Contract rates, which are base linehaul rates like the NTIL, tumbled 5 cents per mile to $2.93/mi. Given the second quarter of 2022 is nearing its end, we can expect to see renegotiations in the weeks to come. These renegotiations, should they take place, will heavily favor shippers and, as a result, contract rates should continue to come down from their current highs.

To learn more about FreightWaves SONAR, click here.

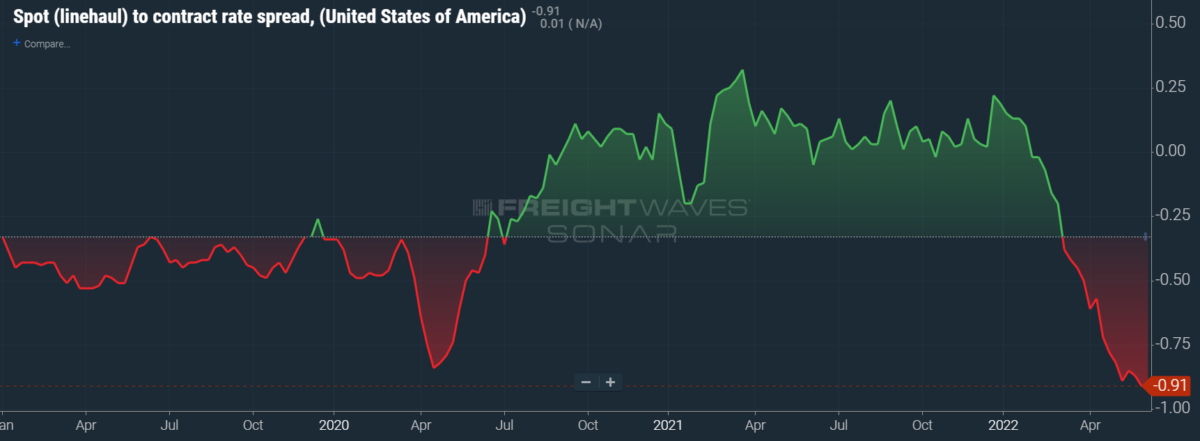

The chart above shows the spread between the NTIL and dry van contract rates, showing the index has continued to fall to new all-time lows in the data set, which dates back to early 2019. Throughout 2019, contract rates exceeded spot rates, which led to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to new record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Once spot rates started the rapid descent from the stratosphere in late February, the spread between contract rates and spot rates narrowed as contract rates continued to increase throughout the first quarter. This caused the spread between contract and spot rates to turn negative for the first time since July 2020.

The spread quickly fell to minus 91 cents, where it stands today. This wide spread will place downward pressure on contract rates as the calendar turns to the back half.

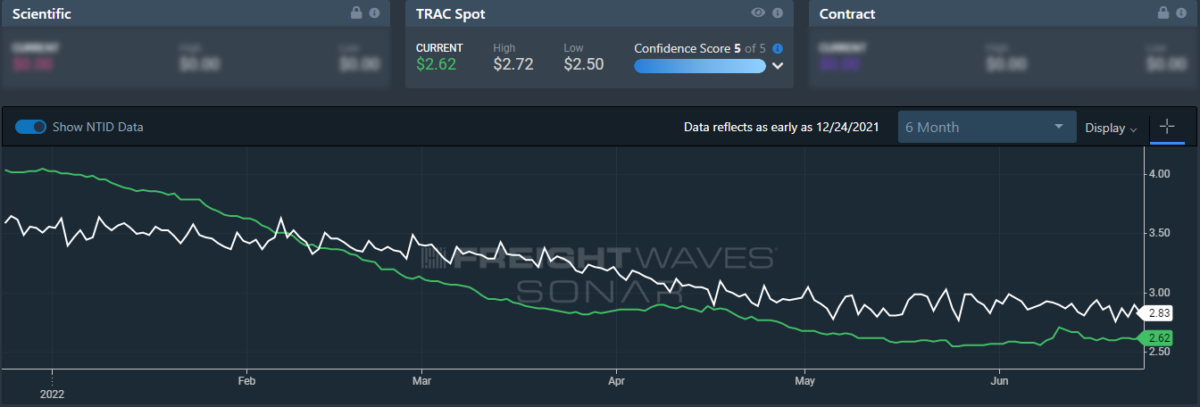

To learn more about FreightWaves TRAC, click here.

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, rose by a small degree. Over the past week, the FreightWaves TRAC spot rate crept up by 2 cents to $2.62/mi. Compared to the NTID, the National Truckload Index – Daily, rates from Los Angeles to Dallas are depressed compared to the national average as expected, but that was not the case at the start of the year. When carriers flooded Southern California in January, they pushed spot rates down rapidly.

To learn more about FreightWaves TRAC, click here.

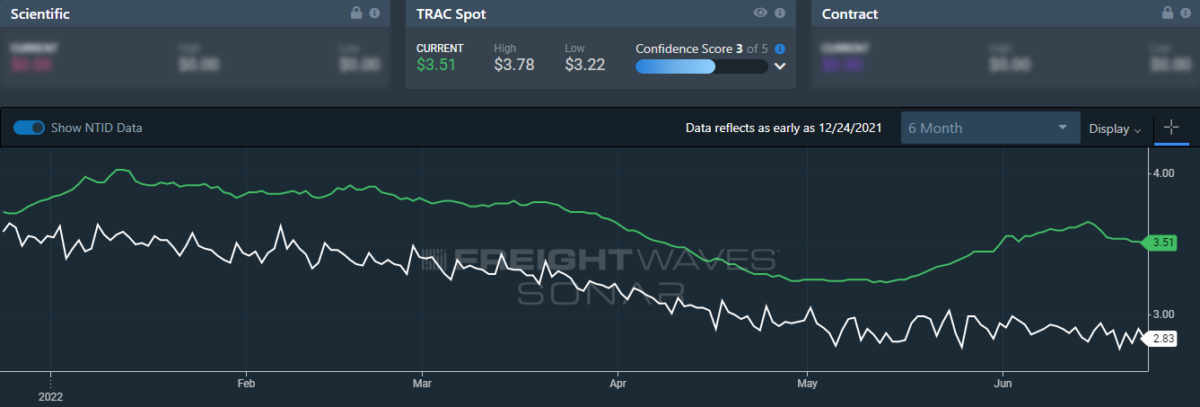

On the East Coast, especially out of Atlanta, rates are falling but are still beating the daily NTI. The FreightWaves TRAC rate from Atlanta to Philadelphia plummeted 9 cents per mile to $3.51, undoing much of the progress made over the past month. Carriers are still showing some restraint heading into the Northeast as diesel prices are extremely high and reserve levels depressed.

For more information on the FreightWaves Passport, please contact Kevin Hill at [email protected], Tony Mulvey at [email protected] or Michael Rudolph at [email protected].