This week’s FreightWaves Supply Chain Pricing Power Index: 40 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 40 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 35 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Volumes fail to rally before Labor Day

Over the past two years, historical trends in freight seasonality have been bucked or otherwise defied to a greater or lesser degree. For instance, the first quarter of 2022 saw feverish activity from shippers when, in previous years, Christmas leftovers were still being digested. Nevertheless, some constants have remained: Most importantly, in the week before a national holiday, shippers will make one final push to get their freight on the road before capacity goes offline.

SONAR: OTVI.USA: 2022 (white), 2021 (green) and 2020 (orange)

To learn more about FreightWaves SONAR, click here.

This week, we did not see a push but instead saw a feeble shrug. The Outbound Tender Volume Index (OTVI) fell 0.04% on a week-over-week (w/w) basis. Some industry watchers (including myself) were hoping for shippers to pull more freight from their sleeves to meet the back-to-school/Labor Day shopping season. But this hope was naive, considering shippers’ inventory woes that have been relayed here countless times.

On a year-over-year (y/y) basis, OTVI is down 22.43%, although y/y comparisons can be colored by significant movement in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

SONAR: CLAV.USA: 2022 (white), 2021 (green) and 2020 (orange)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volume (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a slight rise of 0.03% w/w but also a fall of 4.74% y/y. This y/y difference confirms actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI to lower levels.

August’s jobs report was released Friday, heralding mixed blessings for the labor market. On the one hand, at 315,000, nonfarm payroll growth came in above consensus expectations of 298,000. On the other hand, the unemployment rate hopped to 3.7%, whereas it was expected to remain at 3.5%. Job growth also fell by 211,000 from last month’s revised 526,000. Other key metrics were missed by a hair: Average hourly earnings rose 0.3% m/m and 5.2% y/y against expectations of 0.4% m/m and 5.3% y/y.

In reality, though, the headline figures are neither great nor terrible. Data from the household survey did, however, give pause for concern: The number of multiple jobholders has risen by 702,000 y/y, now constituting 4.7% of all persons employed. More alarmingly, the number of persons working more than one full-time job has jumped 115,000 y/y. When bullish analysts argue against the current recession, they often point to the resilient labor market as defense. But one does not usually see such a swell in people working multiple full-time jobs in an economy that’s purring along, where job applicants can have the proverbial pick of the litter.

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 64 reported weekly increases in tender volume. Among the larger markets, there was both impressive growth and disappointing contraction. Atlanta and Houston, the nation’s second- and third-largest markets by outbound volume, saw freight demand rise 3.46% and 4.67% w/w, respectively. Meanwhile, the largest outbound market — Ontario, California — saw volumes slide 0.78% w/w. This atrophy speaks to shippers’ continued push to East and Gulf Coast ports.

Yet, even for East Coast ports, there might still be trouble on the horizon. The Port of Savannah’s Inbound Ocean TEUs Index (IOTI), which measures the import volume on vessels booked and destined for the port, has fallen 43.5% m/m and is down 58.3% from its peak in mid-May. With an average transit time of nearly 35 days, this collapse in import demand will not make itself apparent to the truckload market for at least two months — possibly longer.

Savannah is not the largest port and has struggled to meet a flood of demand, such that it now has an extensive backlog. On Tuesday, 41 ships were seeking berths in Savannah, accounting for nearly a third of the total vessels waiting offshore that day. Time will ultimately tell whether import volumes trend back to the West Coast or whether they will decline across the board.

By mode: Both reefer and dry van volumes underperformed against the overall OTVI this week. The Reefer Outbound Tender Volume Index (ROTVI) is down 0.29% w/w, signaling the end of the spring-summer produce season. But reefer volumes should, according to historical trends, see an uptick in mid-September that lasts until the end of the year. Harvest season is around the corner, and cold winter weather will necessitate temperature-sensitive goods moving via reefers. ROTVI is down almost 30% y/y, but a large portion of that difference is due to rapidly declining reefer rejection rates.

Van volumes were a bit worse for wear, as the Van Outbound Tender Volume Index (VOTVI) is down 1.27% w/w. Given the much-discussed inventory crisis affecting big box stores and other retailers, a reversal of this decline is not likely in the near future. Similar to reefer volumes, VOTVI is down more than 23% y/y, but the gap is mainly from falling tender rejections.

Rejection rates are largely flat but volatile

On Monday, OTRI dipped down to 5.43% but was able to recover almost all of last weekend’s losses. This time in 2019, when the trucking industry last underwent a recession, OTRI was at 4.81% and was slowly working its way up to its mid-September peak of 6.02%. Now, however, it appears increasingly unlikely that OTRI will trend upward later in the month.

SONAR: OTRI.USA: 2022 (white), 2021 (orange) and 2020 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 5.64%, a change of 7 basis points (bps) from the week prior. OTRI is now 1,738 bps below year-ago levels.

The stage is now set for California’s controversial AB5 law, which reclassifies certain owner-operators as employees rather than independent contractors, to be enforced. The injunction against AB5, which was put in place on the eve of its effective date, has finally been lifted. The California Trucking Association, which had pursued appeals against AB5 that reached the U.S. Supreme Court, reaffirmed its resolve to challenge the law from the beginning. Although the CTA sought another injunction while it prepares to file its briefs, none has yet been granted.

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight, only a few regions this week posted blue markets, which are the ones to focus on.

Of the 135 markets, 72 reported higher rejection rates over the past week, though 49 of those reported increases of only 100 or fewer bps.

Despite suffering from flagging freight demand, the heavyweight market of Ontario saw tender rejections creep up 75 bps w/w, bringing its local OTRI to 2.98%. After posting a local low of 2.19% in mid-May, tender rejections in Ontario appeared to be recovering during the summer. At the start of August, Ontario’s OTRI plummeted, losing 206 bps in two weeks and bottoming out at 2.01%. Last week, its OTRI fell to 1.94% as low spot rates and declining import volumes plagued the market. So while a gain of 75 bps w/w is not incredible by itself, that gain alone represents over a quarter of Ontario’s current OTRI.

To learn more about FreightWaves SONAR, click here.

By mode: For rejection rates, flatbeds are doing quite well but it’s not exactly clear why. While industrial production — a key driver of flatbed freight — was up in July, housing starts were at their lowest level since February 2021 in the same month. Additionally, oil prices have taken a beating since China announced another round of COVID-related lockdowns for the Sichuan city of Chengdu, while Shenzhen (a major electronics manufacturing hub) appears to be next in line.

Nevertheless, the Flatbed Outbound Tender Reject Index (FOTRI) leapt 501 bps w/w to reach 18.3%. Still, FOTRI has fallen far from June’s peak of 32% and is down 604 bps y/y. Reefer rejection rates are also gaining traction despite sluggish demand, as the Reefer Outbound Tender Reject Index (ROTRI) rose 80 bps to 7.5%. Dry van rejections did take a slight tumble, with the Van Outbound Tender Reject Index (VOTRI) falling 24 bps to 5.65%.

Rates inch upward but remain near yearly lows

In the face of dwindling freight demand and tender rejections, both contract and spot rates found a couple of pennies under the cushion this week. Diesel prices are once again on the rise after nine consecutive weeks of decline, with the national average at $5.115 per gallon. Inventories of distillate fuel (which include diesel) are roughly 23% below the five-year average for this time of year. In the Northeast, inventories are 63% under the five-year average, placing upward pressure on rates for lanes headed into the region.

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

This week, the National Truckload Index (NTI) rose 2 cents per mile to $2.67. Half of that bump — that is, a penny — came from higher diesel prices, while the other half was reflected in the linehaul variant of the NTI (NTIL). The NTIL, which excludes fuel costs and other accessorials, gained 1 cent per mile w/w to reach $1.89.

Contract rates, which are base linehaul rates like the NTIL, also gained 2 cents per mile this week to $2.76. In the first two quarters of 2022, contract rates did take severe dips near the end of the first month of the respective quarters — namely, in late January and early April. After falling 25 cents per mile, contract rates were able to recover after a two-week period.

I do not believe that the most recent decline in contract rates is one such dip, as they have been falling since mid-July. Moreover, there are numerous sources of downward pressure on contract rates that were not present in the two previous quarters. Still, it remains a possibility that shippers could be overly cautious about securing capacity and are unwilling to wager for lower rates. If this (unlikely, in my opinion) scenario plays out, we will almost certainly see steeper declines in Q4 2022 and Q1 2023. If the current downturn is more permanent, we are still liable to see these steeper declines.

To learn more about FreightWaves SONAR, click here.

The chart above shows the spread between the NTIL and dry van contract rates, showing the index has continued to fall to all-time lows in the data set, which dates to early 2019. Throughout 2019, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Once spot rates started the rapid descent from the stratosphere in late February, the spread between contract rates and spot rates narrowed as contract rates continued to increase throughout the first quarter. This caused the spread between contract and spot rates to turn negative for the first time since July 2020, as contract rates currently outpace linehaul spot rates by 87 cents per mile.

To learn more about FreightWaves TRAC, click here.

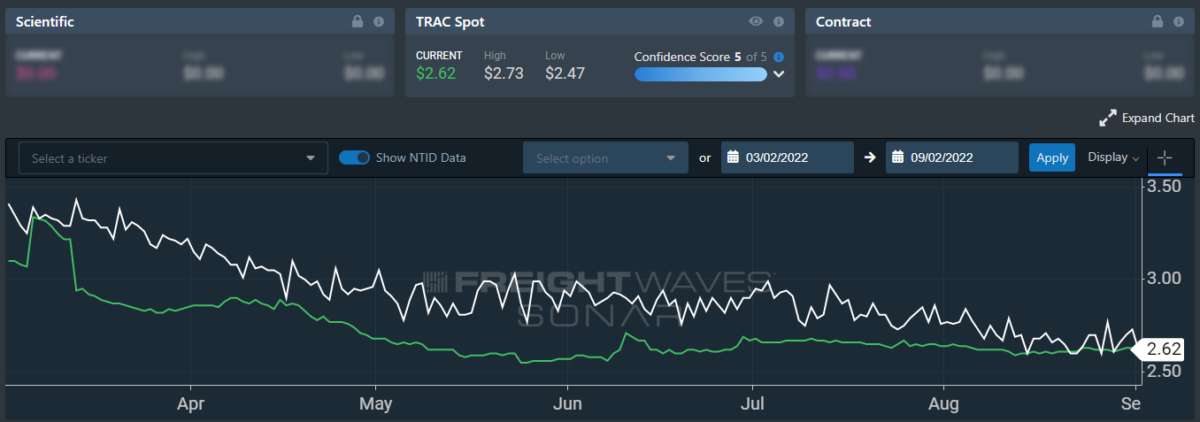

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, seems to have little room to decline further. Over the past week, the TRAC rate remained unchanged at $2.61 per mile. The daily NTI (NTID), which is also at $2.61 per mile, has finally caught up with rates from Los Angeles to Dallas, as the former had consistently outpaced the latter since March.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates did suffer a decline but are still beating the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia fell 8 cents per mile this week to settle at $2.84. Rates along this lane have been falling since mid-July, when the TRAC rate was $3.48 per mile. Low inventory of diesel fuel in the Northeast could soon drive outsized prices, which in turn would place upward pressure on rates to the region.

For more information on the FreightWaves Passport, please contact Kevin Hill at [email protected], Tony Mulvey at [email protected] or Michael Rudolph at [email protected].