This week’s FreightWaves Supply Chain Pricing Power Index: 25 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 25 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 30 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Doves of a Fed-ther?

Signals from the Outbound Tender Volume Index (OTVI) will be a bit erratic until next week, as the holiday noise from Tuesday will be skewing volume levels. Since OTVI is calculated as a seven-day moving average, and since freight demand on the Fourth of July was effectively absent, the current dip should not be alarming by itself.

Nevertheless, demand from retail shippers is historically quiet in the period from now until August, after which retailers restock their shelves for the back-to-school season. But given that many retailers have already noted their reluctance to invest heavily in inventory out of fears for flagging consumer demand, even the traditional peaks of August and September will likely be less “peaky” than usual.

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

OTVI fell an unsurprising (but patriotic) 17.76% on a week-over-week (w/w) basis as holiday noise affects this week’s data. On a year-over-year (y/y) basis, OTVI is down 23.07%, although such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

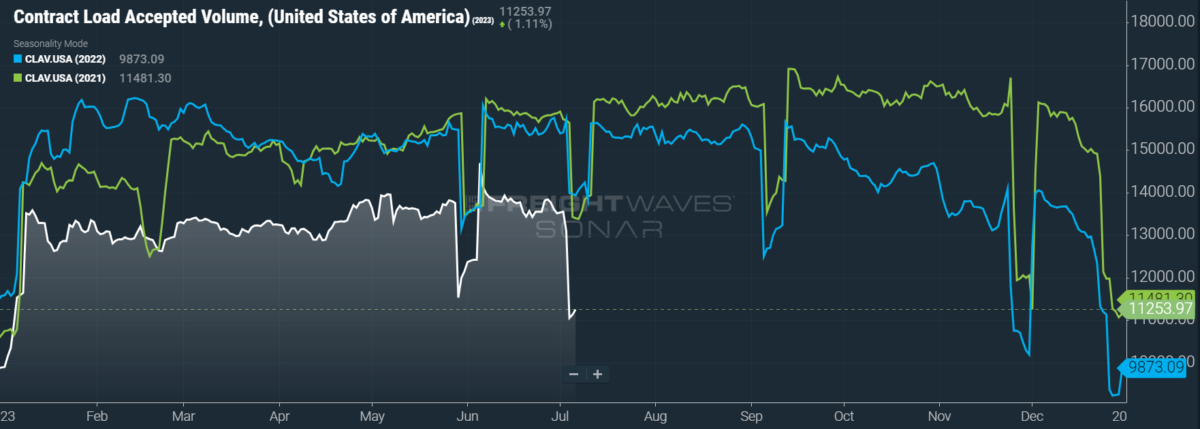

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volume (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a dip of 17.3% w/w as well as a fall of 19.2% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

June data from the labor market appeared this week, with the potential to sway the Federal Open Market Committee to continue its pause of interest rate hikes (or, even better, to knock rates down a notch) at its next meeting later this month. For the first time in 15 months, nonfarm payroll growth came in below Wall Street’s consensus: Compared to the expectation for growth of 225,000 jobs, the Bureau of Labor Statistics reported that only 209,000 jobs were added in June. The unemployment rate did, however, tick down from 3.7% to 3.6% in line with consensus forecasts.

The transportation and warehousing sector took some blows in the June jobs data, as the entire sector lost 6,900 jobs during the month. The warehousing and storage subsector similarly lost 6,900 payrolls, a deficit partially offset by gains in transit and ground passenger transportation (2,100 jobs) and rail transportation (3,200 jobs). The truck transportation subsector, meanwhile, changed little with a loss of 200 payrolls.

Speaking of data that might persuade the Fed to put on a dovish face and loosen monetary policy, the personal consumption expenditures (PCE) index — the Fed’s preferred metric of inflation — was up only 3.8% y/y in June, down significantly from the 5.4% y/y growth seen in January. The effects of federal monetary policy in either direction are slow to affect markets, so it would not be entirely inappropriate for the Fed to ease off the brake and maybe to put its foot on the gas pedal. But such loosening is almost entirely a pipe dream, given previous signaling that another rate hike is on the table for July.

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, only four reported weekly increases as freight demand took a breather on the federal holiday.

Looking at our neighbors (or neighbours) to the north, Canada’s West Coast ports are having a rough go with the International Longshore and Warehouse Union Canada’s Longshore Division. Following the U.S.’ West Coast port scares with the ILWU, which were likely averted by a tentative labor agreement reached on June 14, ILWU Canada is now in its seventh day of striking at the ports of British Columbia. Unlike the ILWU work stoppages at the container import-laden ports of Los Angeles and Long Beach, however, British Columbia’s ports of Vancouver and Prince Rupert are almost entirely disruptive to Canadian exports of bulk cargo.

Accordingly, a coalition of railroads — CN, Canadian Pacific Kansas City and Norfolk Southern — are taking preventive measures to reduce capacity allocations, to implement temporary embargoes and to halt interline shipments to the affected British Columbia ports. While ILWU Canada’s strike might have minimal impact on U.S. freight markets, Canadian shippers might turn southward to push their goods to the nearby ports of Seattle and Tacoma, Washington.

By mode: Given the holiday noise from Independence Day, not much can be said about dry van and reefer volumes this week. California is still suffering from the fallout of late-winter storms and flooding, as the state lacks its usual prominence in outbound reefer volumes typically seen at this time of year. All in all, the Reefer Outbound Tender Volume Index (ROTVI) is down 11.73% w/w — considerably better than the overall OTVI’s performance. The Van Outbound Tender Volume Index (VOTVI), however, is down 19.1% w/w below the general OTVI’s w/w loss.

Rejections see a short-lived bump

After beginning a rally around the middle of June, OTRI was looking like it might sustain some upward momentum for the first time in a long while. But cynics will be unfazed to learn that OTRI’s recent recovery climaxed just before the Fourth of July and that the index is now tumbling. Given the rapidity with which OTRI has fallen, it currently appears that all of June’s gains will be undone in a few days’ time.

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 3.28%, a change of 53 basis points (bps) from the week prior. OTRI is now 383 bps below year-ago levels, with y/y comparisons becoming only more favorable as the year progresses.

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, a few regions posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 45 reported higher rejection rates over the past week, though 33 of those saw increases of only 100 or fewer bps.

To learn more about FreightWaves SONAR, click here.

By mode: Despite having the highest reading among the three modes, it is easy to say that the Flatbed Outbound Tender Reject Index (FOTRI) is in the roughest shape at present. FOTRI, which was almost at 16% at the start of June, has since tumbled back into the single digits. U.S. industrial activity has slowed significantly over the past year and domestic construction might soon take a turn for the worse, leaving FOTRI with few remaining sources of upward pressure. FOTRI is now at 9.29%, having fallen 191 bps w/w.

Reefer rejection rates have dropped back to the levels of early June, but they did not have such an unambiguous rally in that month as van rejection rates did. So, while the Reefer Outbound Tender Reject Index (ROTRI) is down 70 bps w/w, it remains somewhat close to its recent highs. The Van Outbound Tender Reject Index (VOTRI), meanwhile, has shed 61 bps w/w to 3.1%.

Spot is hot, kind of

Unlike OTRI, spot rates have both benefited from the federal holiday and are holding onto those gains — for the time being, at least. While there are few reliable sources of upward pressure on spot rates right now, given the weakness in freight demand and rejection rates, the sheer weight of fundamentals seems to be tipping the scales a bit higher. Obviously, the inflation that has impacted fleet maintenance and insurance costs have made mid-May’s spot rate low of $2.12 per mile unsustainable. But this market has been mired in conditions previously thought unsustainable for longer than expected, so it is refreshing to see spot rates rise again.

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

This week, the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — rose 7 cents per mile to $2.32. Rising linehaul rates were the sole culprit behind this week’s gain, as the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — also rose 7 cents per mile w/w to $1.72.

Contract rates are reported on a two-week delay, but data from late June suggests that they have little inclination to decline further. It will be interesting to see how the federal holiday has impacted contract rates this year since, in 2022, contract rates fell briefly into a divot around July 4. In any case, contract rates — which exclude fuel surcharges and other accessorials like the NTIL — have remained unchanged w/w at $2.39 per mile.

To learn more about FreightWaves SONAR, click here.

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs seemingly weekly, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly early in the year, tightening by 20 cents per mile in January, it has since widened again. Since linehaul spot rates remain 77 cents below contract rates, there is still plenty of room for contract rates to decline — or for spot rates to rise — in the rest of the year.

To learn more about FreightWaves TRAC, click here.

The FreightWaves Trusted Rate Assessment Consortium (TRAC) spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, continues to distance itself from April’s floor. Over the past week, the TRAC rate rose 4 cents per mile to $2.15 — still a distance from its year-to-date high of $2.39. The NTID, which has ticked down to $2.29, is handily outpacing rates from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates have come down a bit but are still outpacing the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia fell 3 cents per mile w/w to $2.64. After a bull run that started at the end of April, this lane has been plateauing above the national average, which is making north-to-south lanes in the East far more attractive than West Coast alternatives.

For more information on FreightWaves’ research, please contact Michael Rudolph at [email protected] or Tony Mulvey at [email protected].

Johnny Freight

Dooms Day’in Freight Waves is back!!